This is an optional stepin the accounting cycle that you will learn about in futurecourses. Steps 1 through 4 were covered in Analyzing and Recording Transactions and Steps 5 through 7were covered in The Adjustment Process. The $9,000 of expenses generated through the accounting period will be shifted from the income summary to the expense account. In this example, the business will have made $10,000 in revenue over the accounting period. In this example, it is assumed that there is just one expense account. LiveCube Task Automation is designed to automate repetitive tasks, improve efficiency, and facilitate real-time collaboration across teams.

Closing Entry: What It Is and How to Record One

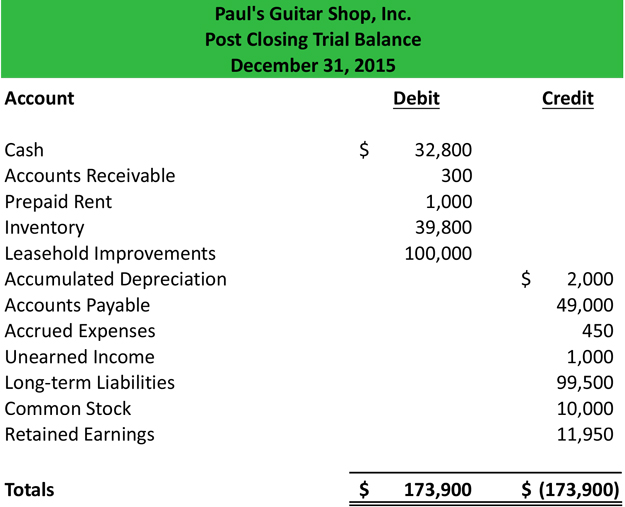

It lists the current balances in all your general ledger accounts. In this case, we can see the snapshot of the opening trial balance below. Keep in mind, however, that this account is only purposeful for closing the books, and thus, it is not recorded into any accounting reports and has a zero balance at the end of the closing process.

Closing Entries Accounting Examples (Beginners:Step by Step)

- LiveCube Task Automation is designed to automate repetitive tasks, improve efficiency, and facilitate real-time collaboration across teams.

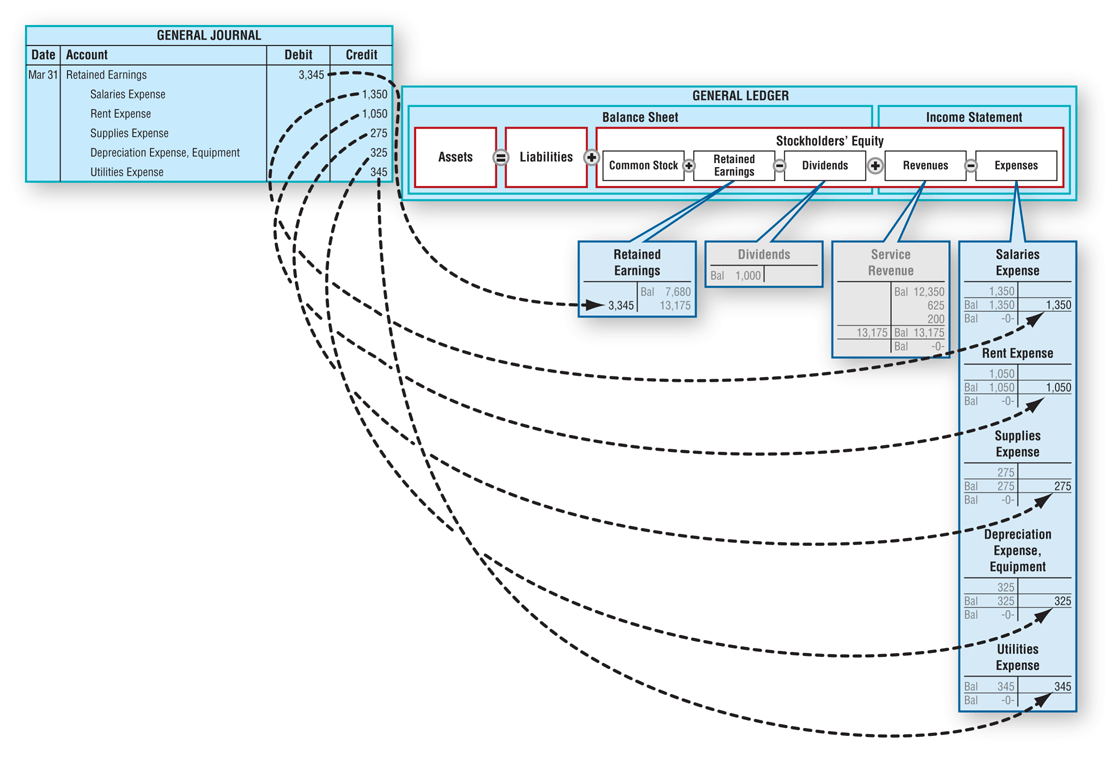

- Now Paul must close the income summary account to retained earnings in the next step of the closing entries.

- This time period, called the accounting period, usually reflects one fiscal year.

- All of Paul’s revenue or income accounts are debited and credited to the income summary account.

- That’s why most business owners avoid the struggle by investing in cloud accounting software instead.

However, some corporations use a temporary clearing account for dividends declared (let’s use “Dividends”). They’d record declarations by debiting Dividends Payable and crediting Dividends. If this is the case, then this temporary dividends account needs to be closed at the end of the period to the capital account, Retained Earnings. When dividends are declared by corporations, they are usually recorded by debiting Dividends Payable and crediting Retained Earnings.

Step 1: Clear revenue to the income summary account

Numeric’s library of templates includes useful examples like an accruals workpaper, an AR recs template, a SaaS close checklist, and much more. While the month-end close process differs greatly from company to company, some procedures — like AP recs and AR recs, for example — remain universal. best invoicing software for small businesses 2021 Here’s a breakdown of the components integral to nearly every company’s close. We evaluate the key components with insights from accounting experts. Debit the Income Summary account and credit each expense account. Debit each revenue account and credit the Income Summary account.

What is Income Summary?

These posted entries will then translate into apost-closing trial balance, which is a trialbalance that is prepared after all of the closing entries have beenrecorded. The $1,000 net profit balance generated through the accounting period then shifts. This is from the income summary to the retained earnings account. The closing journal entries example comprises of opening and closing balances. Opening entries include revenue, expense, Depreciation etc., while closing entries include closing balance of revenue, liability, Depreciation etc. Another essential component of the Highradius suite is the Journal Entry Management module.

Step 1 of 3

Now, if you’re new to accounting, you probably have a ton of questions.

Because this is a positive number, you will debit your income summary account and credit your retained earnings account. Let’s say your business wants to create month-end closing entries. During the accounting period, you earned $5,000 in revenue and had $2,500 in expenses. Without closing revenue accounts, you wouldn’t be able to compare how much your business earns each period because the amount would build up. And without closing expense accounts, you couldn’t compare your business expenses from period to period. On the statement of retained earnings, we reported the ending balance of retained earnings to be $15,190.

Temporary accounts are closed or zero-ed out so that their balances don’t get mixed up with those of the next year. All of Paul’s revenue or income accounts are debited and credited to the income summary account. This resets the income accounts to zero and prepares them for the next year. Temporary accounts can either be closed directly to the retained earnings account or to an intermediate account called the income summary account. The income summary account is then closed to the retained earnings account. Closing entries are necessary to reset the balances of temporary accounts to zero and to update the Retained Earnings account.